Revenue +2,044%, Global IP Expansion Accelerates

Chinese toy brand Pop Mart International Group (HKEX: 9992) delivered record-breaking results in 2025 H1: revenue +204%, net profit +385%. IP expansion including LABUBU, explosive plush toy growth, expanded online channels, and global offline expansion combined to mark a turning point in its evolution toward "China-originated global popular culture brand."

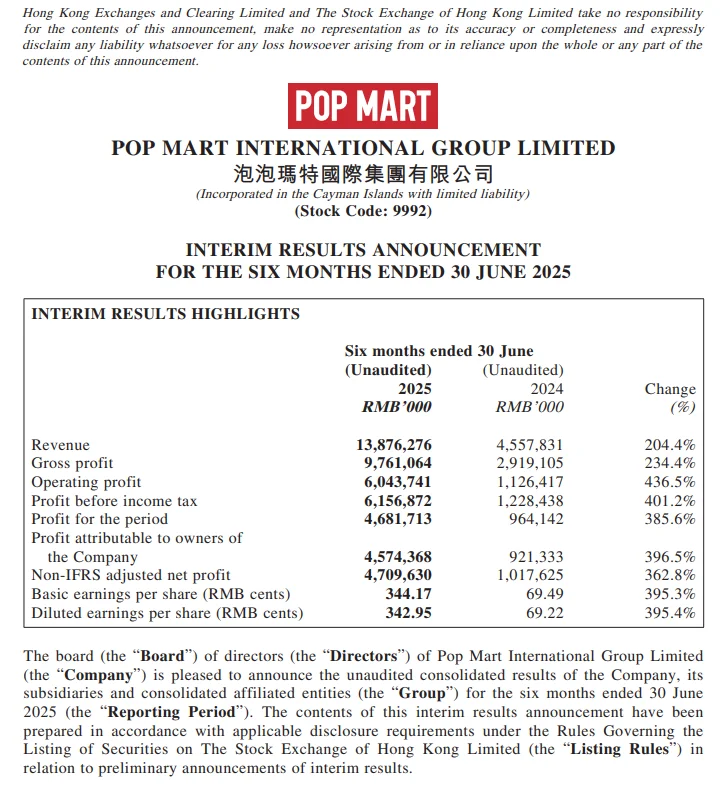

Per the interim report published on the Hong Kong Stock Exchange on August 19: revenue 13.876B CNY (approximately 27T KRW), +204.4% YoY; net profit 4.681B CNY, +385.6%. Gross profit 9.761B CNY, +234.4%; operating profit 6.043B CNY, 4x+; EPS 344.17 CNY cents, +395%. The US market showed +1,142.3% revenue growth and Europe +729.2%.

IP breakdown: THE MONSTERS (including LABUBU) revenue 4.814B CNY, +668%; MOLLY 1.357B CNY; SKULLPANDA, CRYBABY, DIMOO each exceeding 1B CNY. THE MONSTERS alone accounts for over 1/3 of total revenue through global fanbase building. Product mix: plush toys surged from 446M CNY to 6.139B CNY (+1,200%+, 44.2% of total); figures 5.175B CNY (+94.8%); MEGA Collection 1B CNY (7.3%). As of 2025 H1: 571 stores and 2,597 roboshops worldwide across 18 countries; online via TikTok live commerce, Amazon, Shopee, owned app/website. POP LAND theme park in Beijing (opened 2023) hosted "Starlight Summer" events; popop IP-based accessory boutiques opened in Beijing and Shanghai. Cash 11.9B CNY at period end; debt ratio 32.4%. Dividend 1.083B CNY paid (no interim dividend). Strategy forward: IP pool expansion, eco-friendly product development, global offline base expansion. Experts evaluate Pop Mart evolving beyond a simple toy manufacturer to a global popular culture brand, though risks include hit-IP revenue concentration and global consumer spending slowdown uncertainty.